Black Scholes Calculator

One of the essential tools that help option traders set a rational price for stock options is the Black Scholes Calculator India. If you are an active investor in stocks then referring to this Black Scholes Tool guide is very important.

This page will let traders understand what is the black scholes method, how to use the black scholes calculator online, and How to calculate Call options and put options using the Black & Scholes Option Pricing Formula.

Read More:

What is Black Scholes?

A mathematical pattern that assists options traders in calculating the stock options' fair market price is called Black Scholes. You can even call this Black Scholes model as Black-Scholes-Merton (BSM). Fisher black and Myron Scholes developed this BSM in 1973. Later on, Robert Merton was the one to extend the mathematical knowledge of the options pricing model.

The Black-Scholes model is utilized as a guide for traders to make trading decisions by buying options below the formula's value and selling above the determined outcome.

What is a Stock Option? | Types of Options

A stock option is an agreement that bestows the trader a right to buy or sell an asset for a certain amount (means strike price) or before a particular date (means expiry date). You can see two types of options in stocks. They are:

- Call option: It allows the owner to buy the asset at the strike price, and

- Put option: It allows the owner to sell the asset at the strike price.

How Can We Know About The Fair Price To Pay For Options Contract?

Here comes the hero of the guide ie., the Black Scholes Calculator. This tool is the savior for all traders for determining the fair price. BSM applies a partial differential equation to anticipate a stock's price movement in the financial market and reach the price, where one must buy the call or put option.

At this point, you have to use the Black-Scholes formula but all you need to calculate the fair price is the following inputs:

- Spot price means the current price

- Strike price

- Date of Expiry

- Ris-free interest rate

- Expected volatility

- Expected dividend yield

How Do You Calculate the Black Scholes Model Using the Black Scholes Formula?

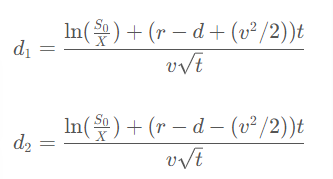

Playing with the calculation of the black scholes model using the formula is a little tricky because the Black Scholes Equation is a difficult mathematical formula. Below, the equations of BSM have been outlined:

C= S e-qt N(d1) - X e-rt N(d2)

P = X e-rt N(-d2) - S e-qt N(-d1)

Where,

C = call option,

P = put option,

S = strike price,

X = current stock price

N(d1) and N(d2) are Cumulative standard normal distribution functions of d1 and d2

q – Dividend yield percentage

r – Risk-free interest rate

T – Term of the option

v – Annualized volatility of the stock

How Does BSM & Black Scholes Calculator Online Work?

When it comes to working with the Black Scholes Model, uses the stock's current price, strike price, volatility, interest rate, and expiry date of a stable asset and calculates the fair price of the stock option. Also, this model accepts that the stock price tracks a lognormal distribution path across the life of the stock option.

When you think about working with BSM Calculator, it follows the three important steps. They are:

- Free Black Scholes calculator gathers the entered input values in the first step.

- Next, it uses the BSM formulas and calculates the price of the stock option.

- Finally, it displays the results on the screen which is a fair price.

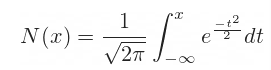

What Are The Formulas Used For Black Scholes In Excel?

The Black-Scholes Option Price Excel Formulas for call option and put option prices are:

C= S e-qt N(d1) - K e-rt N(d2)

P = K e-rt N(-d2) - S e-qt N(-d1)

Both black scholes calculator excel formulas for call and put option prices are identical but contain four terms in each formula. Each term will be calculated separately and then added to the final call and put option formula calculation.

N(d1), N(d2), N(-d2), and N(-d1) terms are unknown parts of the formulas. But N(x) represents the standard normal cumulative distribution function:

Also Read: